Buying a home in the Sunshine State is a dream for many, but once the moving boxes are unpacked, a new reality sets in: Florida property taxes. If you’re moving here from a state with a different tax structure, Florida’s system can feel like a maze of unique terms, exemptions, and “caps.”

At Klosing with Kassidy, we believe a smooth closing is just the beginning for Florida Property Taxes. To help you budget effectively and avoid that dreaded “sticker shock” after your first year of homeownership, let’s pull back the curtain on how the system actually works.

The Basics: What Exactly Are You Paying For?

In Florida property taxes are Ad Valorem, a Latin phrase meaning “according to value.” Essentially, the more your property is worth, the more you contribute to the local community. These taxes are the lifeblood of your neighborhood, funding public schools, police, fire protection, and infrastructure like roads and parks.

However, your bill isn’t just one flat fee. It’s usually split into two parts:

- Ad Valorem Taxes: Based on the value of your real estate.

- Non Ad Valorem Assessments: These are flat fees for specific services like trash collection or street lighting. They aren’t based on your home’s value, but on the cost of providing that service to your lot.

Meet the Players Behind the Bill

At Klosing with Kassidy, to understand your Florida property taxes, you need to know who is pulling the levers:

- Florida Department of Revenue: This state agency ensures every county plays by the same rules.

- County Property Appraiser: This is an elected official who determines the “Just Value” (market value) of your home. They don’t set the tax rates; they just determine the value of the “pie.”

- County Tax Collector: This is the office that sends the bill and collects your money. If you want to pay early for a discount, they’re your go to.

How the Math Happens: From “Just Value” to “Taxable Value”

One of the biggest mistakes new homeowners make is looking at the previous owner’s tax bill and assuming they’ll pay the same. Don’t fall for this! When a home sells, the taxes “reset.” Here is how the math actually works:

1. Just Value

Every January 1st, the Property Appraiser determines the “Just Value” of your home basically, what it would sell for on the open market.

2. Assessed Value & The “Save Our Homes” (SOH) Amendment

This is the “secret sauce” of Florida property taxes system. The Save Our Homes Amendment protects residents from a volatile real estate market. Once you have a Homestead Exemption, the annual increase in your home’s Assessed Value is capped at 3% or the Consumer Price Index (CPI), whichever is lower. This keeps your taxes predictable even if home values in your neighborhood skyrocket.

3. Taxable Value

Your Taxable Value is the final number used to calculate your bill. It’s reached by taking your Assessed Value and subtracting any exemptions you qualify for.

$$Taxable\ Value = Assessed\ Value – Exemptions$$

The Holy Grail: The Florida Homestead Exemption

If you’re making Florida your permanent home, the Florida Property Taxes and Homestead Exemption is your best friend. This isn’t automatic; you must apply through your County Property Appraiser by March 1st.

This exemption can decrease your home’s taxable value by up to $50,000. Even more importantly, it “unlocks” that 3% Save Our Homes cap, providing long term protection for your wallet.

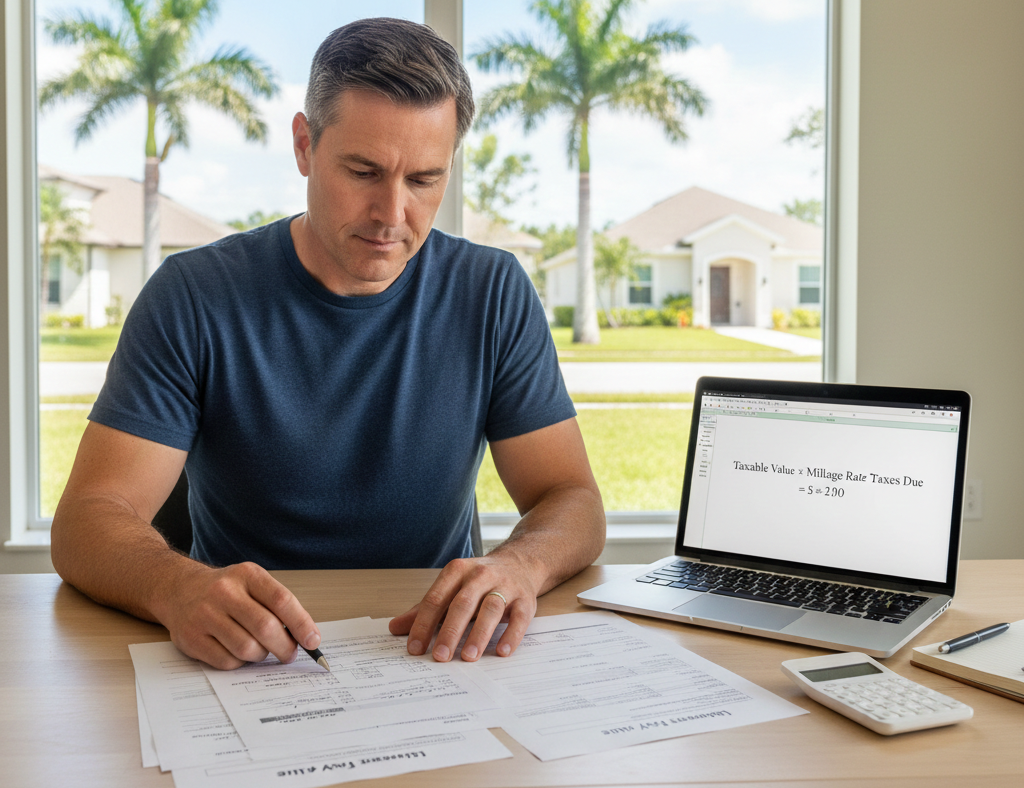

What is a Millage Rate?

When you open your bill, you won’t see a standard percentage. Instead, you’ll see a Millage Rate. One “mill” represents $1 of tax for every $1,000 of taxable value. If your local taxing authorities set a combined rate of 18 mills and your taxable value is $300,000, your tax is calculated like this:

$$(300,000 / 1,000) \times 18 = \$5,400$$

Moving Within the State? Take Your Savings With You

If you’re already a Florida resident and you’re moving to a new home, don’t leave your tax savings behind! Through Portability, you can transfer (or “port”) up to $500,000 of your Save Our Homes tax savings to your new property. This is a massive benefit for families looking to upgrade or downsize without a huge jump in their tax liability.

Dates You Can’t Afford to Forget

- January 1: The date that determines your home’s value and your residency status.

- March 1: The deadline to file for your Homestead Exemption.

- August: Look for your TRIM Notice (Truth in Millage). This isn’t a bill it’s a “heads up” on what your taxes will likely be. This is your chance to protest the value if you think it’s too high.

- November 1: Tax bills are mailed. If you pay in November, you get a 4% discount!

- March 31: The final deadline to pay before taxes become delinquent.

When Things Don’t Seem Right: The VAB

If your TRIM notice arrives and you feel the Property Appraiser got your home’s value wrong, you aren’t stuck. You can petition the Value Adjustment Board (VAB). This is an independent group that listens to your evidence and decides if your assessment should be lowered.

Pro Tip: Use a Calculator

Before you fall in love with a house, use a property tax calculator Florida tool. Most county websites have a “New Homebuyer Estimator.” Because the previous owner’s exemptions and caps disappear when they sell, your taxes will likely be higher than theirs. Checking a calculator for Florida Property Taxes now prevents a budget crisis later. Reach out to us today, and let’s get you close with confidence!

Conclusion

Florida’s property tax system rewards those who stay and make the Sunshine State their permanent home. While the “reset” after a purchase can feel like a jump, the protections offered by the Homestead Exemption and Save Our Homes cap make it one of the most stable places to own a home.

At Klosing with Kassidy, we want you to feel confident every step of the way. Understanding Florida property taxes is a huge part of that.