FHA loans Florida buyers can access in 2026 remain one of the most practical paths to homeownership for first-time buyers, buyers with lower credit scores, and buyers who don’t have 20 percent saved for a down payment. Backed by the Federal Housing Administration and originated by approved private lenders, FHA loans allow down payments as low as 3.5 percent, accept credit scores as low as 580, and provide a viable route to purchase for buyers who don’t qualify for conventional financing at the same income and savings level. If you’re evaluating FHA loans Florida as your path to purchase in the Northeast Florida region, the North Florida real estate market overview shows you where your budget will go furthest before you start the approval process. FHA loans Florida buyers use are not issued directly by the government. The Federal Housing Administration insures these loans against default, which reduces the lender’s risk enough to extend credit to borrowers who wouldn’t qualify for conventional programs at the same income and credit profile. That government backing is what enables the lower down payment and credit score thresholds that make FHA loans Florida’s most accessible mortgage product for entry-level buyers.

FHA loans Florida buyers use are not issued directly by the government. The Federal Housing Administration insures these loans against default, which reduces the lender’s risk enough to extend credit to borrowers who wouldn’t qualify for conventional programs at the same income and credit profile. That government backing is what enables the lower down payment and credit score thresholds that make FHA loans Florida’s most accessible mortgage product for entry-level buyers. Putnam County homes for sale represent the strongest opportunity for FHA loans Florida buyers who want to maximize purchasing power within their down payment and monthly budget constraints. With single-family homes starting around $150,000, the 3.5 percent down payment requirement is as low as $5,250, genuinely achievable for buyers who’ve been saving consistently. Clay County’s entry-level market in Middleburg and western corridor communities is also accessible to FHA buyers, with homes in the $220,000 to $320,000 range fitting comfortably within standard loan limits and representing strong long-term value given the county’s school district quality.

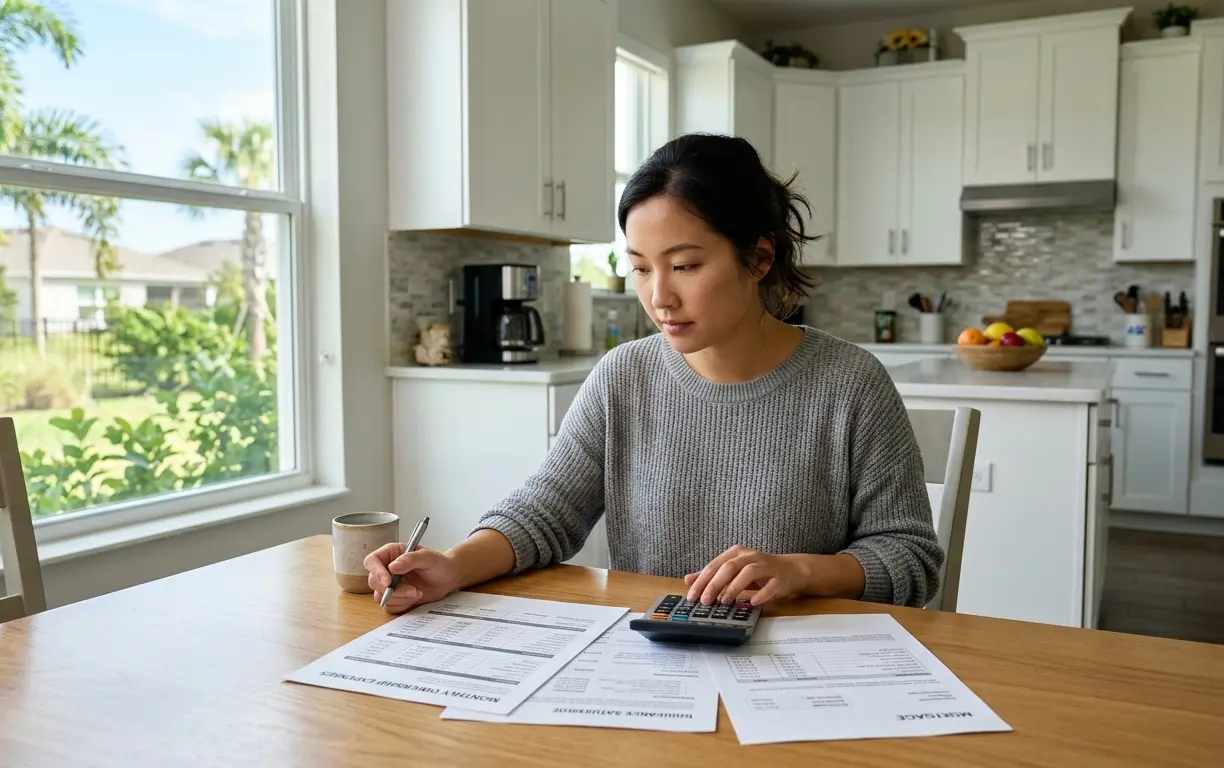

Putnam County homes for sale represent the strongest opportunity for FHA loans Florida buyers who want to maximize purchasing power within their down payment and monthly budget constraints. With single-family homes starting around $150,000, the 3.5 percent down payment requirement is as low as $5,250, genuinely achievable for buyers who’ve been saving consistently. Clay County’s entry-level market in Middleburg and western corridor communities is also accessible to FHA buyers, with homes in the $220,000 to $320,000 range fitting comfortably within standard loan limits and representing strong long-term value given the county’s school district quality. FHA buyers face the same Florida-specific ongoing ownership costs as conventionally financed buyers. Understanding the monthly cost of owning a home in Florida in full detail before committing to a purchase price is critical because the FHA’s lower barrier to entry doesn’t reduce homeowner’s insurance, flood insurance, property taxes, or HOA fee obligations. These costs run $300 to $800 per month or more for many Florida properties and must be factored into the total affordability calculation alongside the mortgage payment and mortgage insurance premium.

FHA buyers face the same Florida-specific ongoing ownership costs as conventionally financed buyers. Understanding the monthly cost of owning a home in Florida in full detail before committing to a purchase price is critical because the FHA’s lower barrier to entry doesn’t reduce homeowner’s insurance, flood insurance, property taxes, or HOA fee obligations. These costs run $300 to $800 per month or more for many Florida properties and must be factored into the total affordability calculation alongside the mortgage payment and mortgage insurance premium.

What FHA Loans Florida Actually Are and How They Work

FHA loans Florida buyers use are not issued directly by the government. The Federal Housing Administration insures these loans against default, which reduces the lender’s risk enough to extend credit to borrowers who wouldn’t qualify for conventional programs at the same income and credit profile. That government backing is what enables the lower down payment and credit score thresholds that make FHA loans Florida’s most accessible mortgage product for entry-level buyers.

FHA loans Florida buyers use are not issued directly by the government. The Federal Housing Administration insures these loans against default, which reduces the lender’s risk enough to extend credit to borrowers who wouldn’t qualify for conventional programs at the same income and credit profile. That government backing is what enables the lower down payment and credit score thresholds that make FHA loans Florida’s most accessible mortgage product for entry-level buyers.Core FHA Loan Benefits for Florida Buyers

FHA loans Florida programs offer several specific advantages that conventional loans don’t provide simultaneously. The 3.5 percent minimum down payment on a $250,000 home means $8,750 at closing rather than the $50,000 required for a 20 percent conventional down payment. Credit scores as low as 580 qualify for the 3.5 percent down payment option. Scores between 500 and 579 require a 10 percent down payment but still qualify for FHA financing when conventional lenders would decline the application entirely. Debt-to-income ratio flexibility is another meaningful advantage, FHA loans Florida lenders typically allow total debt-to-income ratios up to 57 percent in some cases, significantly higher than the 43 to 45 percent conventional limit that excludes many otherwise creditworthy borrowers.FHA Loan Requirements Florida Buyers Need to Meet in 2026

Understanding the full set of FHA loan requirements Florida buyers face in 2026 helps applicants prepare accurately rather than discovering disqualifying factors after they’ve already found a property they want.Credit Score and Income Requirements

The FHA itself sets a minimum credit score of 500 for any FHA loan. Individual lenders apply overlays, additional standards beyond the FHA minimum, that typically push the practical minimum to 580 or 620 depending on the lender. According to the U.S. Department of Housing and Urban Development, the FHA’s official income requirement is not a minimum income threshold but rather a debt-to-income ratio standard that measures monthly debt obligations against monthly gross income. Stable employment history of at least two years in the same field is a standard FHA requirement, and gaps in employment history require documentation and explanation.FHA Loan Limits in Florida’s Four Northeast Counties

FHA loan limits vary by county and are updated annually by HUD. In 2026, the standard FHA loan limit for single-family homes in most Florida counties covers the majority of available inventory in Northeast Florida’s more affordable markets. Putnam County and Alachua County fall within standard limits that align well with local price points. Clay County and St. Johns County, where median prices run higher, may see some higher-priced properties exceed standard FHA limits, requiring buyers to either increase their down payment or evaluate whether the property fits within the conforming limit for their county.What Can FHA Loans Florida Buy in Northeast Florida

Understanding home prices in North Florida 2026 before you calculate your FHA purchasing power gives you a realistic view of what the 3.5 percent down payment option can actually buy across the region’s different markets.Most Affordable Markets for FHA Buyers

Putnam County homes for sale represent the strongest opportunity for FHA loans Florida buyers who want to maximize purchasing power within their down payment and monthly budget constraints. With single-family homes starting around $150,000, the 3.5 percent down payment requirement is as low as $5,250, genuinely achievable for buyers who’ve been saving consistently. Clay County’s entry-level market in Middleburg and western corridor communities is also accessible to FHA buyers, with homes in the $220,000 to $320,000 range fitting comfortably within standard loan limits and representing strong long-term value given the county’s school district quality.

Putnam County homes for sale represent the strongest opportunity for FHA loans Florida buyers who want to maximize purchasing power within their down payment and monthly budget constraints. With single-family homes starting around $150,000, the 3.5 percent down payment requirement is as low as $5,250, genuinely achievable for buyers who’ve been saving consistently. Clay County’s entry-level market in Middleburg and western corridor communities is also accessible to FHA buyers, with homes in the $220,000 to $320,000 range fitting comfortably within standard loan limits and representing strong long-term value given the county’s school district quality.FHA Mortgage Insurance: The Cost Buyers Need to Understand

FHA loans Florida buyers must pay mortgage insurance regardless of their loan-to-value ratio, which is the most important distinction between FHA and conventional financing for buyers who have the credit to qualify for both.Upfront and Annual Mortgage Insurance Premiums

FHA loans Florida programs require an upfront mortgage insurance premium of 1.75 percent of the loan amount, which can be financed into the loan rather than paid at closing. Annual mortgage insurance premiums run 0.55 to 0.75 percent of the loan amount depending on the loan term and down payment, paid monthly as part of the total mortgage payment. On a $250,000 FHA loan, the annual MIP of approximately 0.55 percent adds roughly $115 per month to the total payment. This mortgage insurance cannot be removed from FHA loans originated after June 2013 unless the buyer refinances into a conventional loan once sufficient equity has been built, typically at 20 percent equity.Monthly Costs After Closing on an FHA Loan in Florida

FHA buyers face the same Florida-specific ongoing ownership costs as conventionally financed buyers. Understanding the monthly cost of owning a home in Florida in full detail before committing to a purchase price is critical because the FHA’s lower barrier to entry doesn’t reduce homeowner’s insurance, flood insurance, property taxes, or HOA fee obligations. These costs run $300 to $800 per month or more for many Florida properties and must be factored into the total affordability calculation alongside the mortgage payment and mortgage insurance premium.

FHA buyers face the same Florida-specific ongoing ownership costs as conventionally financed buyers. Understanding the monthly cost of owning a home in Florida in full detail before committing to a purchase price is critical because the FHA’s lower barrier to entry doesn’t reduce homeowner’s insurance, flood insurance, property taxes, or HOA fee obligations. These costs run $300 to $800 per month or more for many Florida properties and must be factored into the total affordability calculation alongside the mortgage payment and mortgage insurance premium.